What If the Angel Market Tanks?

In my last post, I showed how diversification helps an angel portfolio get closer to the true underlying return of the market. Based on the AIPP’s historical sample of angel-backed startups that meet RSCM‘s investment criteria, we saw that 70 investments would have given you a ~90% chance of doubling your money and 200 would have given you an ~80% chance of tripling your money.

Of course, almost everyone has heard the disclaimer, “Past performance is no guarantee of future results.” We don’t really know that angel investments made today will have the same outcome distribution as those made in the past. No amount of statistical wizardy can change that. However, the resampling technique I used in the last post does reveal how a diversified portfolio can provide some protection against losses if the angel market tanks.

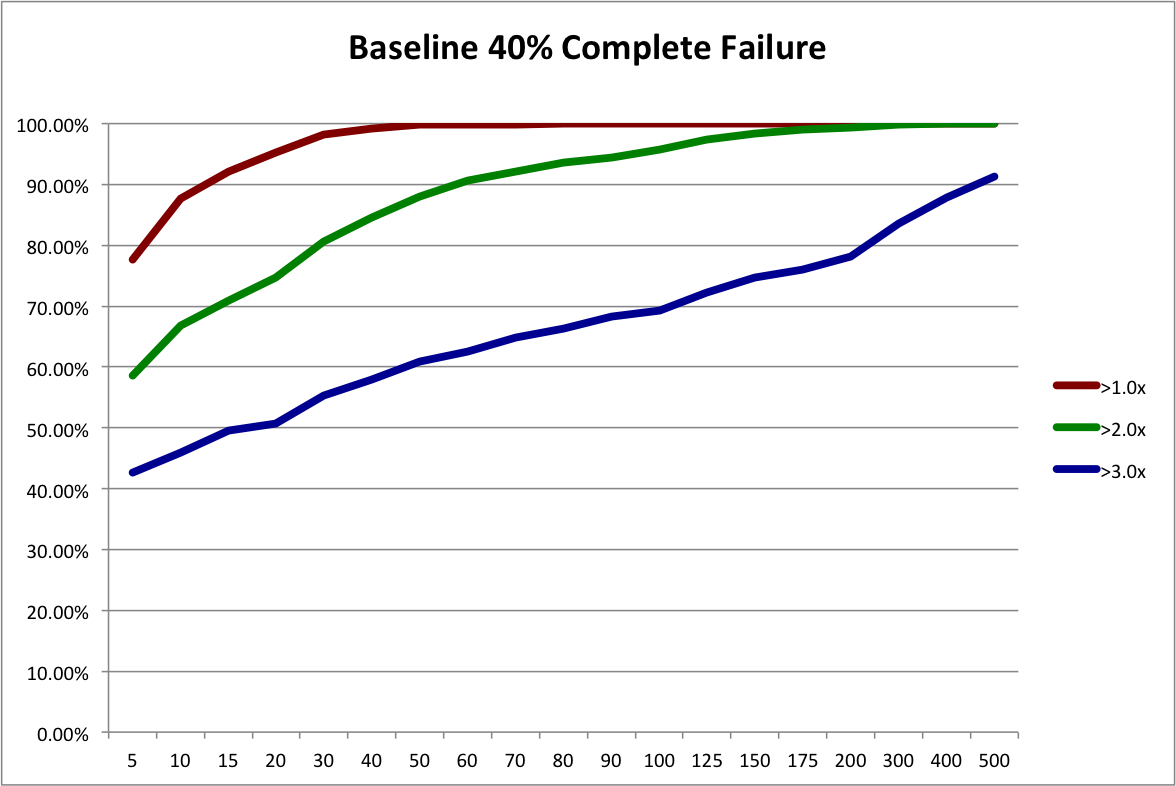

Let’s call a “complete failure” an investment that loses more than 50% of the original capital. Under that definition, the original sample has almost exactly a 40% failure rate: 111 out 277 investments.

So let’s adjust our resampling procedure to simulate different rates of failure in the future. By simply adding in extra copies of the 111 “completely failed” investments, we can see what happens with 50%, 60%, and 70% failure probabilities. Obviously, expected returns decrease as failures increase. But what about the chance of overall loss? Does diversification protect us?

First, let’s refresh our memories with a graph of how different portfolio sizes fare under our baseline scenario of 40% complete failures. Note, that I’ve extended the maximum portfolio size analyzed to 500.

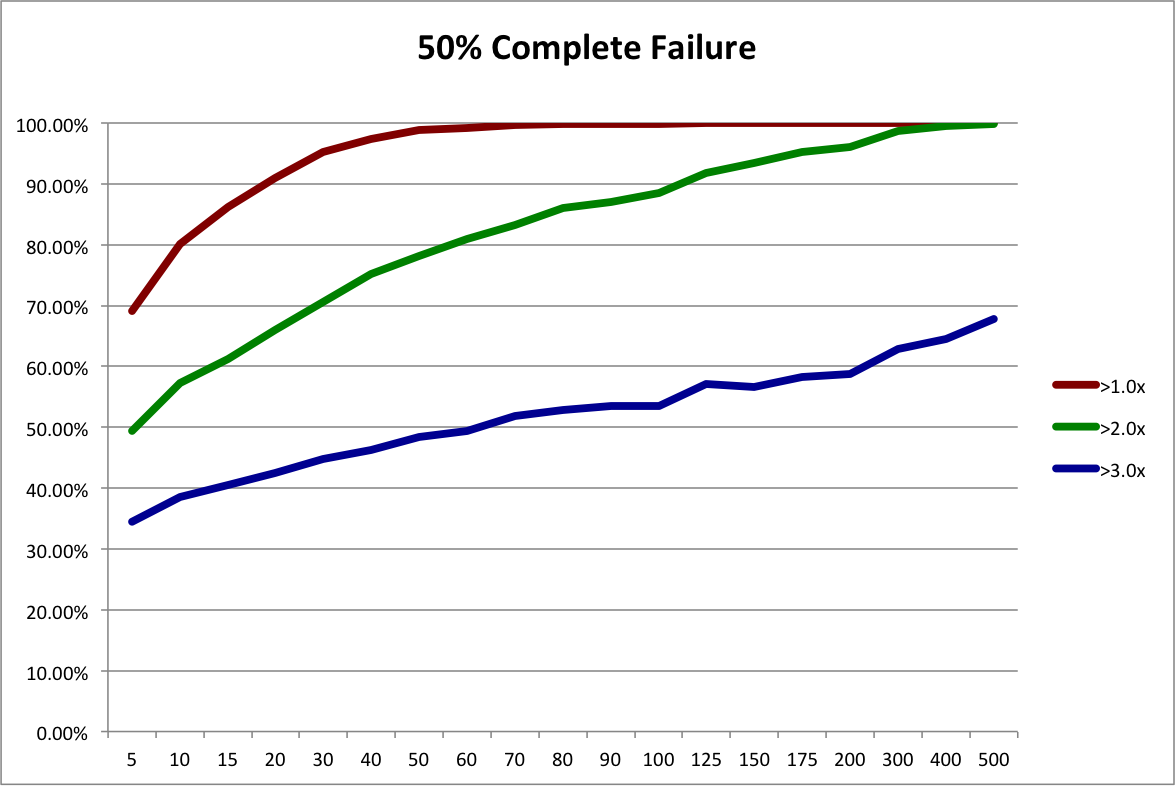

To simulate a 50% failure rate in the future, we start with our baseline sample and add 55 duplicate records of complete failures to create a new sample with a somewhat worse outcome distribution. That makes the failure rate (111+55) / (277+55) = .50. The expected payout is now 3.24x instead of 3.66x. Then we run the resampling procedure on the new sample. The next graph shows the resulting probabilities of achieving 1x, 2x, and 3x the original investment.

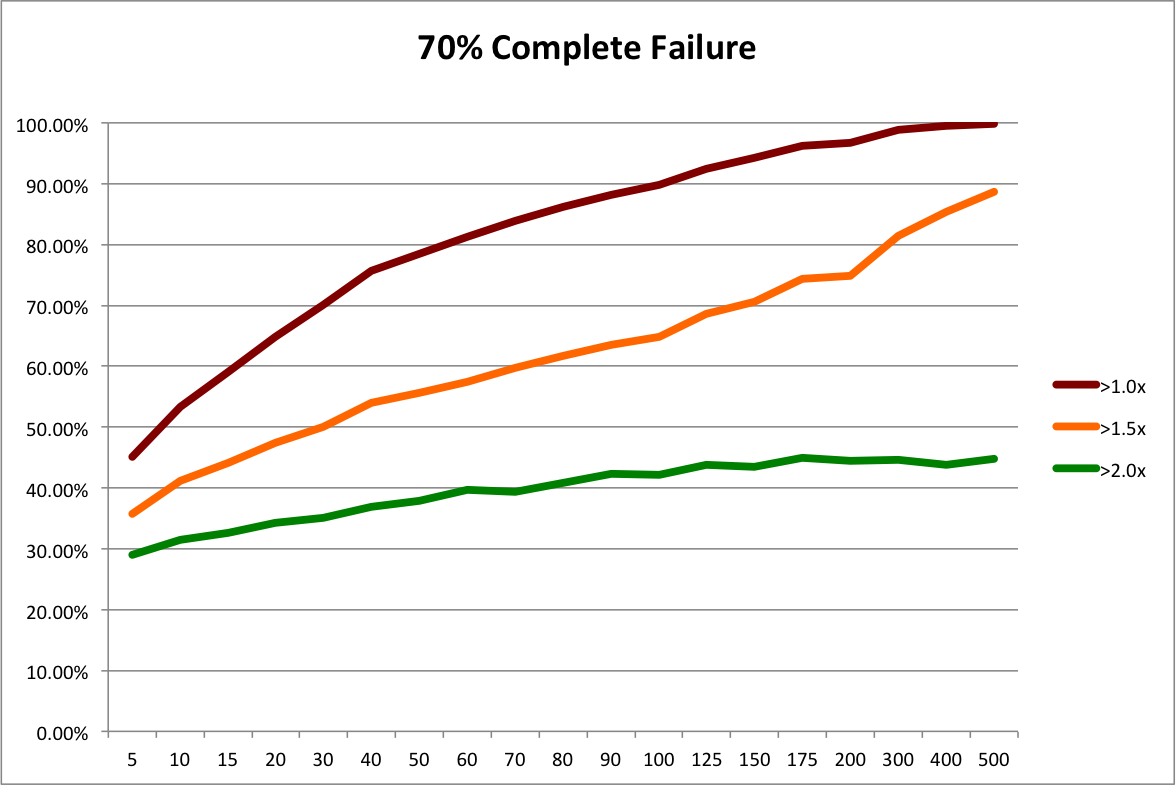

Still not too bad. We’d almost certainly double our money and have a decent chance of tripling. What happens if the angel market really tanks? By adding in more copies of complete failures, we can simulate 60% and 70% failure rates. Expected payouts drop to 2.68x and1.97x, respectively. The next graphs present the probabilities of 1x, 1.5X, and 2x outcomes for these scenarios. 3x is such a remote possibility, I’ve left it out and put in a 1.5X line to give us better resolution.

60% failures isn’t too bad. We can still drive the chance of doubling our money above 90% with 500 investments. 70% complete failures sucks. Especially when you look at it from the perspective of homeruns. Remember that big winners drive returns. If a “homerun” is any investment with at least a 10x return, adding in all the complete failures drops the percentage of homeruns from from 7.6% in the baseline to 3.8% in the worst case. So in some sense, the market is only half as good. Even then, a portfolio of 200 investments has less than a 5% chance of losing money and a portfolio of 500 investments has less than 1% chance. Diversification still provides decent protection.

Also consider that the most likely cause of such an awful angel market would be macro events that affect the entire economy. The NASDAQ and S&P 500 would probably not be doing well either.

I think this analysis shows that diversification is a good idea even if you think the future angel market may fluctuate. This conclusion isn’t at all surprising. Fundamentally, diversification reduces volatility. If you think the future market might differ from the past market, that means you believe the market is more volatile. Therefore, diversification is actually more important.

[Note added 4/3/2013: here is the Excel file I used for these simulations.]

[Updated 4/25/2013: corrected minor error in spreadsheet and graphs.]

thanks for validating our investment thesis. avg sample size per fund is ~250 companies.

DMC

Dave McClure

April 2, 2013 at 8:45 pm

You’re welcome Dave. Great minds and all that 🙂 250 investments per fund is excellent. We’re on track to hit about that level and I’m quite pleased.

Kevin

April 2, 2013 at 10:24 pm

[…] data analyses from my last two posts, How Many Angel Investments? and What If the Angel Market Tanks?, have an important alternative interpretation. If you also read my earlier posts on […]

Angel Investing: Diversification vs Skill | Possible Insight

April 9, 2013 at 6:31 pm

[…] playing with the data from my previous angel diversification posts (here, here, and here), I developed the best visualization so far of how to improve your angel portfolio with […]

Visualizing Angel Diversification | Possible Insight

April 25, 2013 at 9:57 pm