Archive for May 2015

Full Year 2014 “Seed Bubble” Update

According to my usual data sources, 2014 was not nearly as good a year in seed funding as I would have expected from reading news reports. I was fully prepared to see “bubbly” data. However:

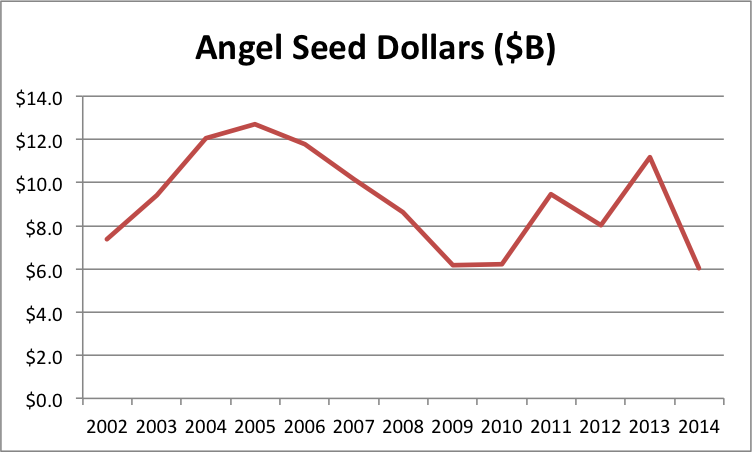

- From angels, seed stage funding plunged nearly 50%, from $11.2B to $6.0B.

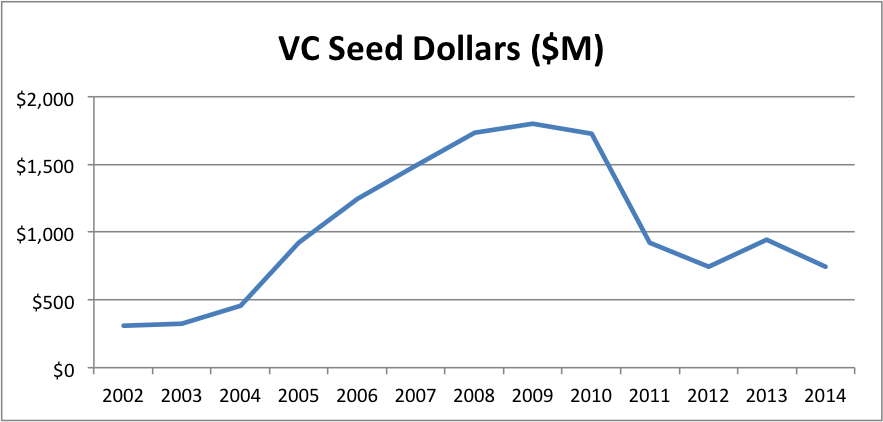

- From VCs, seed stage funding dropped about 25%, from $940M to $740M.

(While VC early stage jumped over 60% and expansion stage spiked over 110%.) - But median seed valuations increased 20%, from $2.5M to $3.0M.

The run up of a bubble does not typically include sharp volume drops, but the price rise may indicate something interesting is going on.

See here, here, here, here, here, here, and here for previous posts in this thread. My data sources are the Center for Venture Research for angel data, the NVCA for VC data, and my personal tracking spreadsheet for “super angel” funds not part of the NVCA. I use the HALO report for pricing data.

Out of concern that one possible explanation for individual angel investments dropping is a shift to angel funds, I reconstructed my angel fund tracking spreadsheet from scratch. I was worried that my list of funds was too haphazard. So I pulled a longer, hopefully more complete, list of micro VC firms from CB Insights. I then removed ones that are members of the NVCA, whose investments should already be included in that data. I also went through fund CrunchBase listings and Web sites, filtering out those who invest primarily outside the US or not at the seed stage. I noted the reason for any such exclusions in my latest spreadsheet. This updated source contains 74 funds totaling $3.2B, while my 2013 source contained 29 funds totaling $1.2B—a substantial increase in coverage. There were also 23 funds on the new list for whom I could not find dollar amounts. However, I assume each fund with dollar amounts is completely deployed in the current year so the total should still be a gracious estimate given that even very fast funds actually deploy over two or three years.

Despite the addition of $2B in covered super angel investments, the 2014 graphs were still sobering with a 25% total volume drop year-over-year:

The big question is how do you get a pronounced volume drop and a pronounced price increase? First, one of the data sources could have a problem. The obvious candidate here is the CVR angel data because it accounts for most of the total volume I track, the methods aren’t documented, and this is its biggest one-year drop ever. According to the latest report, total angel investment volume was only down 2.8%. But the proportion of seed and early investment plummeted from 45% to 25%. I can think of several reasons for a potential measurement inconsistencies here. Note that the 2012 measurement was 35% so it has a lot volatility.

Similarly, the CB Insights pricing data could be the result of an anomaly, as it also experienced its biggest one-year move. In contrast to CB Insights’ 20% jump in valuations, the CVR valuation data showed a slight decrease across all stages (but the CVR valuation data is reported inconsistently, so I have avoided using it in the past). Of course, the CB Insights and CVR data collection methods could somehow result in systematically different samples that explain the conflicting data.

There’s another explanation that I find tantalizing, if only because it would confirm my hypothesis that founder opportunity cost drives the earliest company valuations. Think of seed stage companies as “supplying” investments and investors “consuming” them. Econ 101 says that a simultaneous decrease in volume and increase in price implies that the supply curve has shifted left. It’s like a freeze wiping out a significant fraction of the orange crop. People buy less at higher prices because there’s a shortage. But why would this happen now in the seed stage startup market?

I have a guess: the macroeconomy recovered. Unemployment eased from 7.5% in June 2013 to 6.1% in June 2014. Moreover, according to Indeed.com, software engineering salaries jumped 20% in 4Q2013. All of a sudden, the opportunity cost of founding a seed stage startup went up dramatically. That could definitely have an effect on formation rates, which would show up first in the seed stage funding data. Another “supply side” explanation would be that founders simply need less money to advance their ideas past the seed stage. The total number of angel-funded deals actually went up 3.8% according to the CVR report.

At RSCM, we’ve certainly seen no shortage of quality opportunities at low valuations. If anything, we are deluged. Of course, we purposely focus on smaller deals so we wouldn’t expect to see any shortage if lower capital requirements were the underlying cause. Our experience is also consistent with a data collection anomaly. I’d love to get my hands on a good dataset for accelerator program application volume. That might allow us to distinguish between declines in formation rates and capital requirements.

Bottom line: I’m still very skeptical that there is a seed stage bubble.