Archive for January 2014

Seed Bubble Watch 1st Half 2013

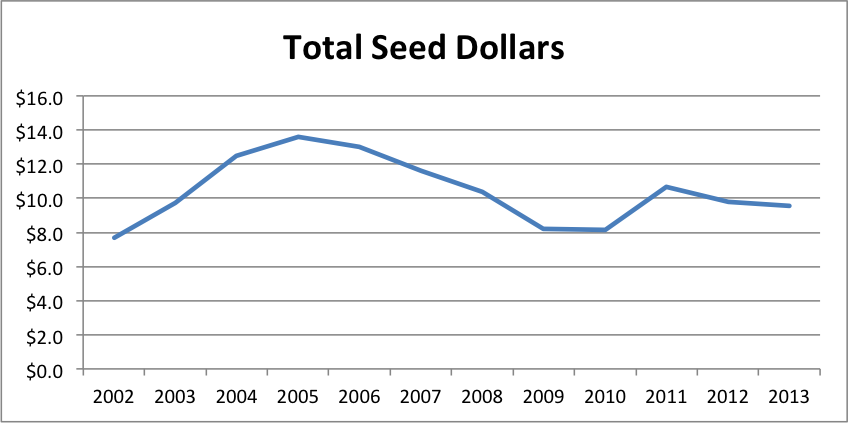

Well, it’s been almost three years since I started watching for quantitative evidence of a “bubble” in seed-stage technology funding. I feel like a broken record saying there’s still no sign. Here are the highlights:

- 1H2013 volume is 30% below the 2005 global maximum

- 1H2013 volume is 10% below the 2011 local maximum

- Seed stage valuations have been flat since 2011

You simply don’t have a bubble when volume is down and prices are flat!

To review the history of my seed bubble watch, see here, here, here, here, and here. Recall that I use the Center for Venture Research’s angel data, the NVCA’s VC data, and my personal list of “super angel” funds not part of the NVCA. The volume calculation methodology is not designed to produce the most accurate estimate of the true number of seed-stage dollars. Rather, I want it maximally sensitive to sudden influxes in new seed money. I use the HALO report for pricing data, which started coming out in 2011.

That said, here are the graphs (spreadsheet here):

The story continues to be that traditional VCs have become increasingly irrelevant as their seed dollars have dropped 60% from 2009 to 1H2013 and their share of all seed dollars has plunged from 22% to 7.5%.

Angel’s position has gradually eroded from 2011 to 2013, with their share decreasing from 88% to 77%. Super angels and seed funds have gained in share during that time, jumping from 3.0% to 15%. My guess is that trend will continue unless the individual angel pool increases via new platforms like AngelList. In any case, the new breed of funds is not growing fast enough yet to make up for decreases from other sources.

[Edit 8pm: Somehow this paragraph got deleted from my draft.] There also appears to be no pricing pressure at the seed stage. According to the 2012 and 2Q2013 HALO reports, the median seed-stage pre-money valuation has remained $2.5M since 2011. Moreover, the 25th and 75th percentile valuations have actually decreased, making it hard to argue that there is some hidden dynamic masking a buildup in prices.

Interestingly, the HALO report shows a continued drop in California’s share of angel group activity. From 21.0% in 2011, to 18.1% in 2012, to 17.3% in 1H2013. I’ll take this as continued confirmation that RSCM is right that some of the best values are outside the Bay Area.

It will be interesting to see what the data shows for 2H2013 and 1H2014. With the S&P reaching new highs throughout 4Q2013, institutions should increase their allocations to alternative investment funds and angels should feel like they have more wealth to invest in startups. Assuming the public markets don’t experience a sudden drop in the beginning of 2014, of course.