Full Year 2013 “Seed Bubble” Update

So there are finally some signs if life in seed-stage technology funding:

- In nominal terms, we roughly equaled the global peak from 2005.

- Seed stage valuations have remained flat since 2011.

- Adjusting for the size of the economy and our wealth, the level is still down.

Kind of hard to call this situation a “bubble”. But I can live with calling it a “recovery”.

Once again, see here, here, here, here, here, and here for previous posts in this thread. My data sources are the Center for Venture Research for angel data, the NVCA for VC data, and my personal tracking spreadsheet for “super angel” funds not part of the NVCA. For super angel investment, I worry most about detecting new chunks of money, not necessarily measuring the “true” level. I use the HALO report for pricing data, which goes back to 2011.

Here are the graphs (spreadsheet here):

It looks like all the components are recovering, though traditional VC somewhat more slowly and super angel somewhat more quickly. The question is still, “Bubble or no bubble?”

Let’s look at prices, as I did in my 1H2013 post. According to the full year 2013 HALO report, the median seed valuation is still $2.5M… just like 2012… and 2011. The 75th percentile valuation is up slightly in 2013, from $3.7M to $4.2M. But the 25th percentile valuation is down a hair from $1.5M to $1.4M. According to the methodology described in the report, this data includes angel group deals before Series A. So what I think is happening is that some companies that might have gone for a VC round in the past are doing a larger angel round instead. If you check out my spreadsheet, you can see that check sizes for what the NVCA calls “seed” have taken another swing up, probably pushing some early startups out of that market. So no obvious pricing pressure.

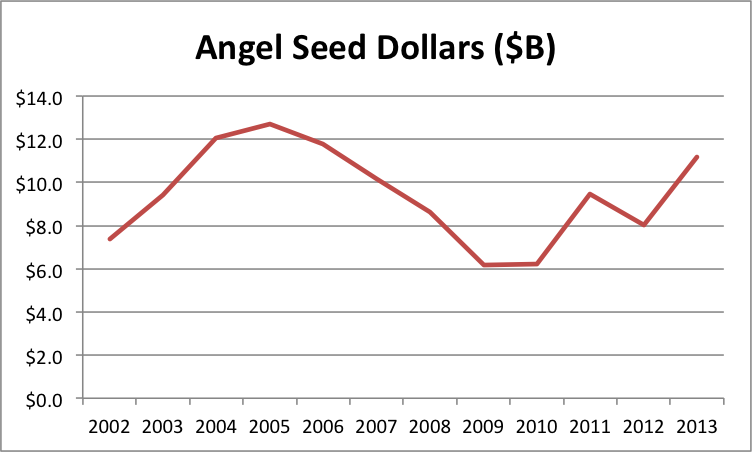

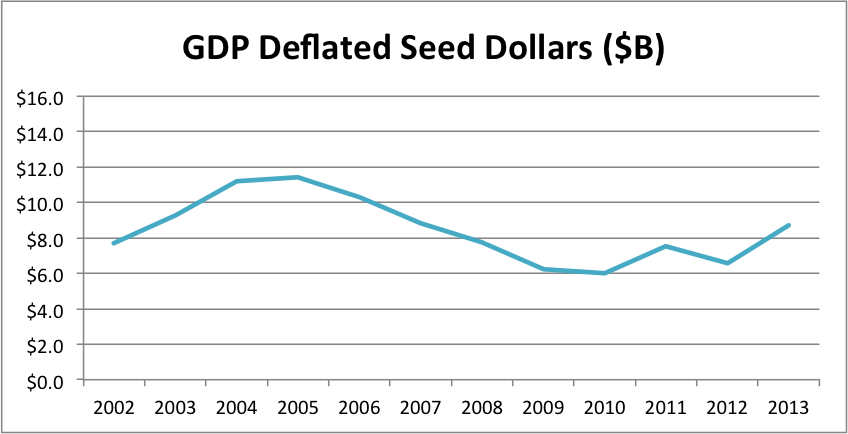

Moreover, I think the following graphs make a bubble quite unlikely. I’ve been waiting for years to pull these out. The first one “deflates” the seed investment levels by adjusting for GDP. Thus it measures how seed investment has changed relative to total economic output. The second one deflates seed investment levels by adjusting for the level of the S&P500 index (on July 1 of the given year). Thus it measures how seed investment has changed relative to the total stock of wealth.

Compared to our economic output and total wealth, seed-stage investment seems like it still has a significant amount of headroom. I’m actually pretty sure I could build a darned accurate forecasting model based mostly on the S&P. Given that the index is up roughly 25% from July 2013 to July 2014, my eyeball estimate is that 1H2014’s numbers will show us somewhere around a $16B annual rate.

[…] here, here, here, here, here, here, and here for previous posts in this thread. My data sources are the Center for Venture Research for angel […]

Full Year 2013 “Seed Bubble” Update | Possible Insight

May 27, 2015 at 7:58 pm